“Data assimilation, optimization and applications”

Ulaanbaatar (Oulan Bator), Mongolia

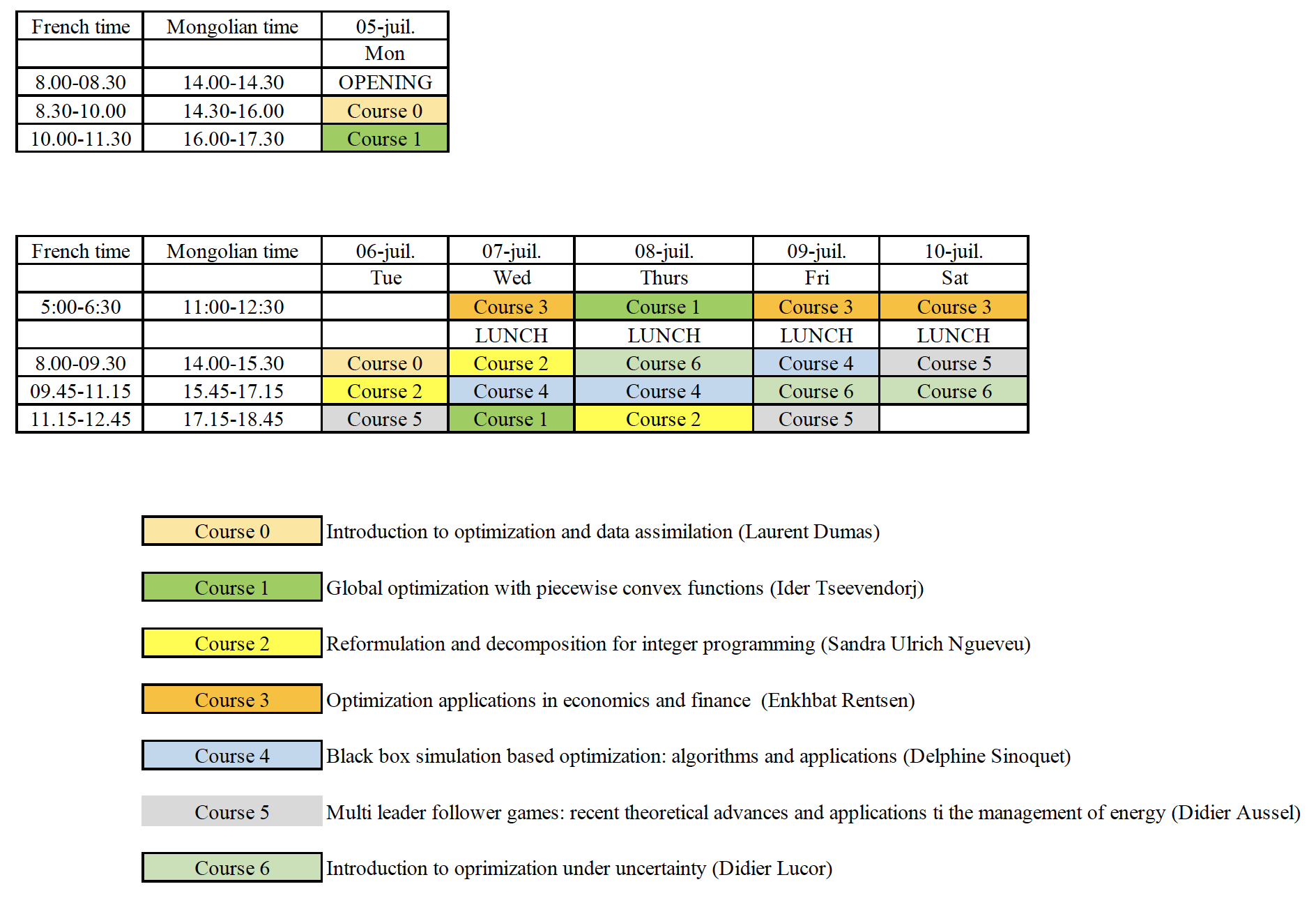

2021, July 5th- July 10th

Optimization problems are encountered in many fields (engineering, finance, economics) and can lead to various mathematical formulations: convex or nonconvex type function, blackbox function, integer or continuous type and with various constraints.

The objective of this CIMPA school is to present various topics in the field of optimization and data assimilation in order to solve such applied problems.

Host institution

Established in 2013, German-Mongolian Institute for Resources and Technology (GMIT) is the youngest state university and the first university in Mongolia based on bilateral governmental cooperation. The German Federal Government supports the University’s continued development. GMIT shall provide a model for the reform of higher education in Mongolia.

Being a university for scientific teaching and research, GMIT strives to serve Mongolia by educating highly qualified, socially responsible, internationally recognized technology experts and by advancing research and innovation for the benefit of society. It is guided by German excellence in science and technology and has a firm grounding in Mongolia’s culture and heritage. Teaching and research are characterized by strong practice-orientation and dedication to foster creative, critical thinking. The language of instruction is English.

Local coordinator:

Altangerel Lkhamsuren, GMIT ()

External coordinator:

Laurent Dumas, Versailles University ()

Courses

Six courses will take place during this school. They all deal with various aspects of optimization and will often be linked with a particular application (finance, energy, …).

An introductory course on optimization(basic theory in convex analysis, standard numerical tools like gradient based or gradient free methods, etc…) will also be given during the first two days of the conference.

Each course is divided into three talks of one hour and a half. Complementary computer sessions and work sessions in small groups of students will also be organized at the end of the afternoon. Currently, GMIT has two PC pools equipped with 25+10 computers.

List of courses:

ONLINE: “Multi-leader-follower games: recent theoretical advances and applications to the management of energy” (Didier Aussel, Perpignan University)

ONSITE: “Optimization Applications in Economics and Finance” (Enkhbat Rentsen, National University of Mongolia)

ONLINE: “Introduction to optimization under uncertainty” (Didier Lucor, LISN Lab, Paris Saclay University)

ONLINE: “Reformulation and decomposition for integer programming” (Sandra Ulrich Ngueveu, Toulouse University)

ONLINE: “Black-box simulation based optimization : algorithms and applications” (Delphine Sinoquet, IFPEN agency)

Note that a preliminary registration is mandatory for entering the conference.

Detailed description of courses (and slides)

Course 0:

Title: “Introduction to optimization and data assimilation” (Laurent Dumas)

Abstract of the course: an introductory course on basic tools in optimization and data assimilation will be given. It will present the main notions in the field of optimization (convex theory, gradient based or gradient free optimization methods, constraints handling) and data assimilation (Kalman filtering) that will be used in the school courses.

Title: “Global optimization with piecewise convex functions” (Ider Tseevendorj)

Abstract of the course: the main investigation in these lectures is concerned with a piecewise convex function which can be defined by the pointwise minimum of convex functions:

F(x)=min { f1(x),…,fm(x)}.

Such piecewise convex functions closely approximate any continuous function, that seems to us as a natural extension of the piecewise affine approximation from convex analysis. Maximizing the function F(x) over a convex domain have been investigated during the last decade by carrying tools based mostly on linearization and affine separation. In these lecture, we present a brief overview of optimality conditions, methods and some attempts to solve this difficult nonconvex optimization problem. We will study relationships such nonconvex optimization problem with other optimization related problems. We will also present new approaches of solving the nonconvex problem, which is based nonlinear separation ideas.

Title: “Reformulation and decomposition for integer programming” (Sandra Ulrich Ngueveu)

Abstract of the course: Integer linear programming solvers have become remarkably efficient thanks to recent advances such as the integration of automatic generation of valid inequalities, preprocessing, heuristics and advanced exploration strategies. As a consequence, a widely used approach for solving various optimization problems is to reformulate them into integer linear programs. In spite of these developments, the exploitation of the specific structures of the problems remains up to the user.

In this course, we will review the methods allowing to reformulate problems into integer linear programs exploiting their structures. The goal is to obtain a significant reduction of the computing times and guarantees on the quality of the solutions obtained. We will then focus on algorithms based on piecewise linearization of nonlinear functions and Dantzig-Wolfe decomposition. The course will be illustrated with cases studies from transportation, network design and energy optimization.

Title: “Optimization Applications in Economics and Finance” (Enkhbat Rentsen)

Abstract of the course: optimization plays an important role not only in science and technology, operations research but also in economics and finance. This serie of lectures discusses applications of optimization theory and methods in economics and finance. The purpose of these three lectures is to reveal applications of optimization theory and methods in economics and illustrate these on some examples of Mongolian economy. They include various areas of economics such as Solow growth model, consumer theory, game theory, cost minimization, investment and population models, and also mathematical model for insurance.

Title: “Black-box simulation based optimization : algorithms and applications” (Delphine Sinoquet)

Abstract of the course: optimization takes place in many industrial applications: inferring the parameters of numerical models from experimental data (earth sciences, combustion in engines, chemical process), design optimization (wind turbine, risers, networks of oil pipelines), optimizing the settings of experimental devices (calibration of engines, catalysis). These optimizations consist in minimizing a functional that is complex (nonlinearities, noise, depending on heterogeneous types of variables) and expensive to estimate (solution of a numerical model based on differential systems, experimental measurements), and for which derivatives are often not available, with nonlinear constraints, and sometimes with several objectives among which it is necessary to find the best compromise.

In this course, we focus on black-box simulation based optimization problems or Derivative Free Optimization problems (DFO). The first talk is dedicated to the main classes of methods and algorithms of Derivative Free Optimization. The second talk illustrates some various applications of DFO in geosciences, new energies, chemistry and transport domains. The third talk introduces some challenging ongoing research subjects to tackle some specific but recurrent difficulties encountered in practical black-box optimization problems: uncertainties, mixed continuous discrete variables, “hidden” constraints…

Title: “Multi-leader-follower games: recent theoretical advances and applications to the management of energy” (Didier Aussel)

Abstract of the course: this course is divided in three talks. In the first talk, we consider a game where a set of players is split into two groups: the leaders and the followers. A Multi-leader-follower game between these players is then a generalized Nash game between the leaders for which the optimization problem of each leader depends on the solution set of a Generalized Nash games between the followers. Our aim will be to recall the basic properties of Bilevel optimization and Nash games optimality conditions will be considered as well as algorithms. A motivating example in the management of energy (electricity market or industrial eco-park) will be used to introduce the formal definition of a Multi-leader-follower game (MLFG). In the second talk, we will bring to the fore the main possible ambiguities/ill-posedness of MLFG and the remedial adaptations. The theoretical properties of two special cases (Single-Leader-Multi-follower game and Multi-Leader-Single-Follower game) will be presented: existence of solutions, reformulations… as well as the numerical analysis already developed in the literature to solve these difficult problems. The third talk will be dedicated to applications to energy management applications: electricity market, Industrial eco-park, contract problem in energy exchanges. Numerical results will be commented and some insights on the « stability » of such solutions will be discussed.

Course 6:

Title: “Introduction to optimization under uncertainty” (Didier Lucor)

Abstract of the course: the course is divided in three talks. The first talk is devoted to an introduction to random processes and random fields: in probability theory, stochastic processes are infinite indexed collection of random variables, defined over a common probability space. The index parameter is typically time or a spatial dimension. Important aspects of random processes such as dependencies of the random variables of the process, long-term averages, extreme or boundary events will be introduced in order to understand how it can be used for random process estimation and detection as well as model construction. Stochastic processes fundamentals will be necessary to follow the two other lectures. The second talk deals with Gaussian process surrogate models: for some computer experiments, the repeated evaluation of a functional is computationally prohibitive, so it is tempting to replace the complex model by a simpler and cheaper surrogate model. To this end, conditional Gaussian process models (Kriging) used to interpolate a dataset will be introduced as well as the way it is possible to sequentially enrich the initial database with interesting data. Finally, the third talk will present the main tools of optimization under uncertainty (OUU) also related to reliability based design optimization (RBDO). A special emphasis will be given on the use of adaptive metamodeling approaches such as Kriging-based approaches in the case of costly function evaluations.